May 2015

May 2015

The purpose of the African Development Bank (AfDB), founded in 1964, is to provide capital to alleviate poverty, improve living conditions and spur economic and social development. It is the largest external funder of infrastructure in sub-Saharan Africa.1 Under the astute leadership of Donald Kaberuka, the Bank has demonstrated resilience and ability to co-ordinate appropriate continental responses to external threats. In 2009, a doubling of loan and grant approvals to US$8 billion helped to mitigate the effects on Africa of a global recession. The following year, shareholders approved a threefold increase of the AfDB’s capital base.

The Bank has forged partnerships with the private sector to fund investment in infrastructure, which it regards as the basic requirement to accelerate economic growth and encourage foreign direct investment and regional trade. It has established itself as a leading source of knowledge on development, provider of technical expertise and trusted advocate for the interests of a continent undergoing rapid change and economic growth.

On 27 May, the Board of Governors will elect a new president at its 50th annual meeting. With donor finance static since the global financial crisis, there are constraints in the Bank’s funding model. Its non-African shareholders demand that the Bank take on more complex roles than traditional project lending. With limited resources, the AfDB is being called upon to lead on issues where it either lacks experience or will find it hard to demonstrate success, including the development of post-conflict and fragile states, regional integration, trade negotiation, gender equality, climate change and infectious disease control. Kaberuka’s successor will face a difficult task.

Back from the brink

In the mid-1990s, the AfDB was engulfed by scandal and near-bankruptcy due to bad lending and corruption. Repair of the balance sheet was the main preoccupation during the presidency of Omar Kabbaj. When former Rwandan finance minister Kaberuka succeeded Kabbaj in 2005, the Bank was providing only 6% of total aid to Africa – less than the United Kingdom. Its international standing was low. Some donors questioned its continued existence.

In 2006, a panel of experts convened by the influential Washington-based Center for Global Development recommended that the principal role of the AfDB should be to promote economic growth through private sector development, regional trade integration and better economic management; and that it should specialise in infrastructure development. The advice on major regional and global issues – for example, climate change – was “lead but don’t lend”.²

The backdrop was unpromising. Africa’s economic growth was subdued and the continent had largely been bypassed by a substantial expansion in global trade and investment. Regional integration was a failure. The Bank was in danger of being crowded out by larger, external donors such as the World Bank and European Commission. But Kaberuka’s arrival coincided with a significant improvement in Africa’s economic performance.

Fuelled by demand for its natural resources, growth in South-South trade and the flow of capital from developed to emerging and frontier markets, by 2013 Africa had become the world’s second fastest-growing region. The AfDB benefited substantially from – and built on – this change of fortunes. It returned to its origins as primarily a funder of infrastructure and its 2013-22 strategy articulated a determination to “place the Bank at the centre of Africa’s transformation”.

An infrastructure bank with a wider remit

According to AfDB estimates, Africa requires infrastructure investment of nearly US$100 billion a year for a decade in order to generate broad-based annual average GDP growth of 7%. At present, only half that sum is being spent. Among other projects, the AfDB has co-financed the Kazungula road and rail bridge linking Botswana, Zambia and Zimbabwe; roads from eastern Nigeria to western Cameroon and between the capitals of Mali and Guinea; and the Turkana wind farm in Kenya, the largest of its kind in eastern Africa.

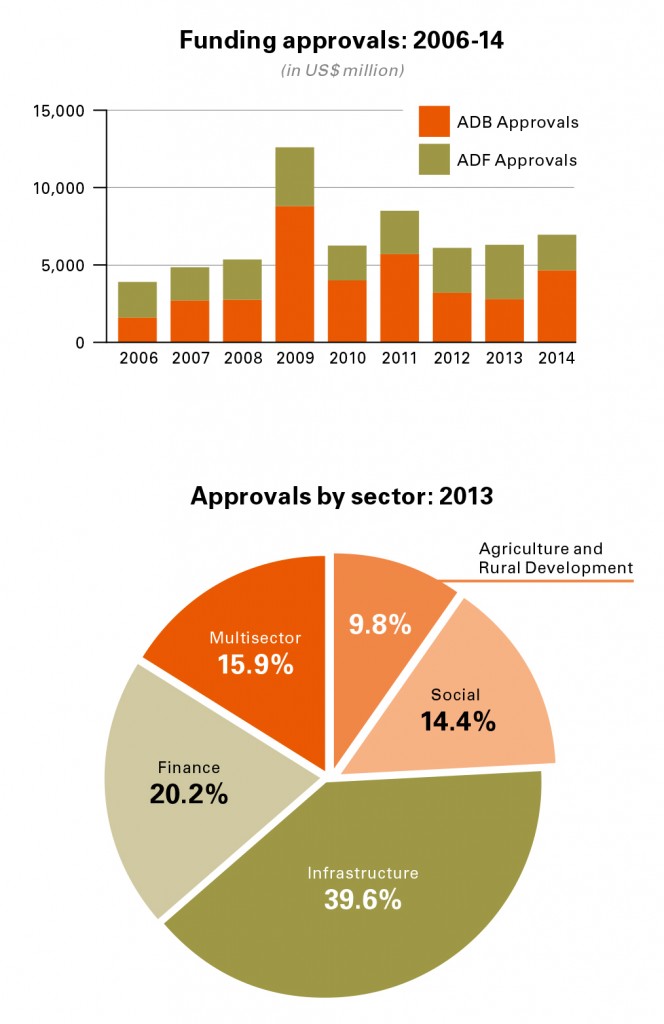

At US$4-5 billion a year, the Bank’s lending meets a fraction of Africa’s infrastructure and development needs. Financing the mega-projects desired by many governments, such as power stations and transport corridors, is not possible alone. “We have to be clever, doing more with less, and so does Africa,” says an AfDB spokesperson. “The only way to make an impact is through partnerships.” Every US$1 the Bank lends to public sector projects helps to raise another US$3 from other donors or private sector investors, a ratio it aims to increase to 1:10.

Partnerships with the private sector and acceleration of regional integration are priorities: private sector lending exceeds US$1.5 billion a year, a tenfold increase since 2006, with energy and transport projects accounting for two-thirds of commitments. Since 2006, the Bank has co-ordinated 50 public-private partnerships (PPPs). It sees its role as one of facilitating private investment by improving the feasibility, and reducing the regulatory and other risks, of projects: risk mitigation lowers borrowing costs. In 2010, it also set up a loan syndication unit, which has lent more than US$4 billion financed by commercial lenders alongside the Bank. Joint funding spreads risk and makes limited resources stretch further: for example, US$373 million was raised for Dakar’s integrated power and transport project, with the AfDB contributing less than 20% of funding.

In its drive to accelerate infrastructure investment, the AfDB has assumed a role in a plethora of initiatives with a similar objective. It is the executing agency for the Programme for Infrastructure Development in Africa, a scheme of the New Partnership for Africa’s Development (NEPAD) Secretariat and African Union Commission for regional and continental infrastructure and services. It is co-financing projects promoted by Power Africa, a US-led plan to add 30,000MW of electricity-generation capacity. Through its Africa50 Infrastructure Fund, the Bank is seeking to channel African currency reserves and savings into infrastructure projects that it is prevented by its AAA credit rating from co-funding directly.

New and unpredictable demands stretch the Bank’s human and financial resources

Flexibility is crucial. “We’ve got a client base whose demands are changing rapidly, especially regarding infrastructure finance,” says Kapil Kapoor, AfDB’s director of policy and strategy. Several initiatives have raised the AfDB’s profile as a knowledge bank and advocate for the continent, such as the African Financial Markets Initiative – a “gateway to Africa’s bond markets” – and the African Legal Support Facility. This helps governments to negotiate complex commercial transactions, deal with asset-seizure threats by hostile creditors and build their own expertise in these areas. It is currently advising on more than US$18 billion-worth of transactions, including a recent iron ore deal between the government of Guinea and mining company Rio Tinto.

New and unpredictable demands stretch the Bank’s human and financial resources. It supported Guinea, Liberia and Sierra Leone as they battled to contain the Ebola epidemic, distributing US$223 million to fund nine operations in the region, launching a response fund alongside the African Union, the Economic Commission for Africa and private sector donors, and contributing an additional US$300 million to transport and infrastructure improvement.

In 2015, the Bank is co-ordinating Africa’s stance at the UN Climate Change Conference and on the sustainable development goals, which will determine the global development agenda for the next 15 years. Member countries are being encouraged to include gender equality in all programmes. “We recognise that these issues are vital to development. But the President has said that we cannot do everything, we must act as an honest broker and a catalyst for change,” says a Bank spokesperson.

African Development Bank Group key facts:

African Development Bank Group key facts:Constraints and opportunities

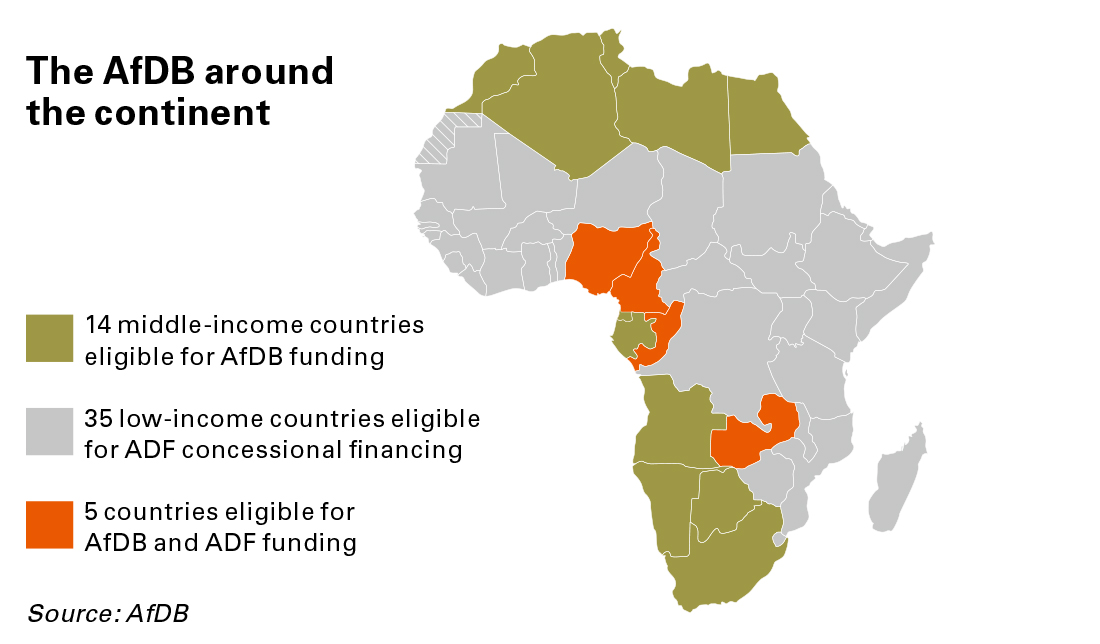

The AfDB’s prudence has protected its AAA credit rating and helped to secure the capital increase in 2010. It also dictates that most lending be allocated to Africa’s 14 middle-income countries; half of its loans are to North Africa. Thirty-four low-income countries are only eligible for about one-third of AfDB resources, through the concessional “window” of the African Development Fund (ADF), which provides grants and interest-free loans. Five countries can access Bank lending and ADF funds.3 In 2004-13, the Bank disbursed approximately US$27 billion to low-income countries through the ADF, substantially funded by non-African member countries, whereas it lent US$36 billion to middle-income countries in the same period. The ADF’s budgeted lending for 2014-16 is US$7.4 billion, a 22% reduction on the previous three year window and equivalent to just US$2.5 billion per annum to address the needs of 39 countries.

The growing mismatch between the AfDB’s structure and the needs of most countries in Africa was highlighted in a recent internal policy review. Strong growth and sound macroeconomic management have enabled many countries to attract commercial loans and foreign direct investment, which now exceed aid as the continent’s main source of finance.4 Some, not all of them in the middle-income category, have been able to access international debt capital markets. Traditional donors no longer hold exclusive sway.

Bank insiders recognize that its model has to change

“The Bank has in the last year or two had difficulty finding people to whom it can lend,” a senior representative of a leading shareholder told ARI. “The North Africans have exhausted what they can borrow. Others like Namibia, Botswana and Angola don’t want to borrow from the AfDB. Meanwhile, the ADF’s pot has been declining, so the amount it can give to the poorer countries in concessional funds is quite small – much smaller than the World Bank. This is a problem when the AfDB is claiming to be the main institution on the continent. Some of the poorer countries want to become non-concessional [i.e. commercial-rate] borrowers. But we have to be careful we don’t create bad debtors in Mozambique, Ethiopia and similar countries.”

Bank insiders recognise that its model has to change. It has sought to encourage multilateral donors to invest in fragile and post-conflict states, an area in which it wants to assume a growing role but acknowledges a lack of capacity at present. All multilateral development banks, including the World Bank, are reassessing their relevance. Well-established international finance institutions are being challenged by new institutions like China’s Asian Infrastructure Investment Bank. “No one here will tell you the AfDB is no longer needed, but we can’t go on being generously funded by the international donors,” says a spokesperson.

There are opportunities. Partnerships with private investors and companies keen to invest in African infrastructure and developing economies are one. “Parallel funding” arrangements with sovereign states that cannot increase their investment in the AfDB due to the strictures of its capital structure are another. In January 2014, Japan pledged to double to US$2 billion its support for the AfDB’s Enhanced Private Sector Assistance for Africa initiative, which supports entrepreneurship and job creation. In May 2014, China and the AfDB launched a new 10-year co-financing facility, the Africa Growing Together Fund, to be run alongside the Bank’s existing lending operations.

African central bank reserves, institutional savings and pension funds are further underutilised resources for development. The AfDB is actively encouraging African governments to use their domestic private sector to provide infrastructure through PPPs and other schemes. It has helped to persuade the South African government to increase the amount its pension funds can invest elsewhere in Africa, a move it says will add billions of dollars in continent-wide investment. The Bank is also keen to tap sovereign wealth funds and pension funds globally. “They want good long-term projects and African infrastructure offers many. The trick is to match long-term investors with Africa’s long-term infrastructure needs”, says Kapil Kapoor. “If the projects are seen as too risky, we try to work out how to lessen the risk.”

The outlook for Kaberuka’s successor is more promising than it appeared in 2006, but it is likely to be equally unpredictable

Governance and a new president

The growing influence of emerging economies has led to pressure to change a governance structure that has altered little since non-African members became shareholders in 1982. Unlike the World Bank and IMF, shareholdings are not based on global economic weighting and remain fixed until the Bank’s next fundraising. “China wants to increase its shareholding and would like to have a permanent executive director – it’s currently in a constituency represented on the board by Canada – but cannot do this until there is a capital increase,” says the senior representative of one shareholder. “India too has a commercial interest in the AfDB and would like to increase its shareholding.”

A new injection of funds is unlikely to occur in the foreseeable future. While it would enable the Bank to lend more to middle-income countries and the large economies of North Africa, it would make no difference to those only eligible for concessional ADF funds. “There is far less of a case for a capital increase in the AfDB than in the Inter-American Development Bank or the Asian Development Bank,” says the shareholder representative, who regards the Bank’s performance as mixed. “The AfDB is generally easier to deal with than the World Bank, but less able to do what it says it will do. Kaberuka hasn’t shown the leadership that we wanted on getting the Bank to deliver results. The African Natural Resources Center in Ghana [established as a non-lending entity to provide expertise to the Bank and member countries] is not up and running. Africa50 is going through teething troubles. There have been so many initiatives, partly as a result of pressure from regional members, to be fair.”

The shareholder representative commends the Bank for “getting to grips with fragile states” and for its role in advocating increased domestic spending on AIDS, tuberculosis and malaria prevention in Africa. “We expect to see more of that”, he adds. “New issues – women, girls and sustainable development – are becoming increasingly important.” As the Bank enters a new era, with its return to its original home in Abidjan, Côte d’Ivoire, this is a reminder that its management has to balance countless, sometimes conflicting – and seemingly increasing – demands from its shareholders and member countries. The shareholders’ 20 executive directors are resident at the Bank’s headquarters, a set-up not replicated by the Asian Development Bank, for example, and one that is unlikely to change.

The outlook for Kaberuka’s successor is more promising than it appeared in 2006, but it is likely to be equally unpredictable. The one-off boost from debt relief is over, as for the time being is the resources boom. Government borrowing is on the rise5 and GDP growth across the continent is slowing as external demand weakens. Job creation, health and education provision, and savings and investment rates have all failed to keep pace with growth. If Africa is to reap a demographic dividend, rather than succumb to a demographic shock, investment must be channelled towards social and infrastructure needs and consolidating growth in low-income economies. Retaining and defining a central role for the AfDB and financing it will require great skill, leadership and improved delivery on the part of its new president over the next decade.